Occam’s – Is the Value Premium Pining for the Fjords?

There’s no magic formula for investing. The financial markets seem to take some sort of cosmic joy in bringing people back down to Earth. And it’s value investing’s turn – in fact, it’s been value investing’s turn for a while now. To put it mildly, this has been a rough decade and a half for value stocks.

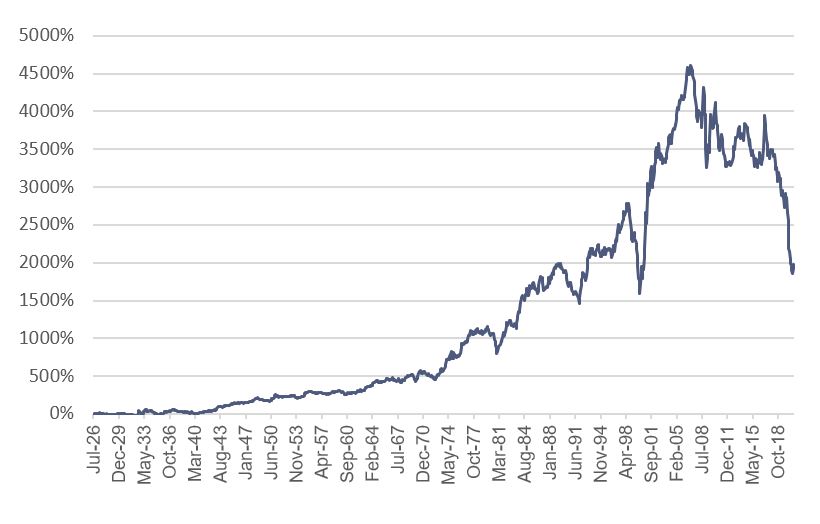

This has been the worst period for the value premium that we have ever seen. Rather than belabor the numbers, I think one chart can sum it up pretty well.

Cumulative Return of the Fama/French US Value Factor 7/1926 – 11/2020

For education purposes only. Past performance is no guarantee of future returns. Indices are not available for direct investment.

This is a chart of the cumulative returns of the value premium – the difference between the returns of value and growth stocks. The story is clear – this has been an ugly decade and a half for value stocks.

And it’s led a lot of people, quite reasonably, to start asking is value dead? And additionally, is there a premium for owning growth stocks now?

Before we start looking at the current situation, let’s rewind a bit and talk a little about what the value premium actually is. Put simply, the value premium is the idea that the stocks that the market doesn’t “like,” value stocks, have better long-term returns than those stocks that the market “likes.”

So let’s take apart what this actually means. The price of a security is determined by how much investors are willing to pay for it (on both sides of the trade – both the person buying and selling a security need to be happy with the trade). When we are talking about value stocks, we’re specifically talking about stocks where investors aren’t willing to pay much relative to some fundamental measure of the company’s operations.

This means that investors are demanding a higher expected return for holding value companies. A good way to think about this is to look at how investors price securities. Effectively, the price of a security is the current value of all of it’s future cash flows.

Basically, if you’re looking at two stocks with the same expected future cash flows, but Stock A’s price is lower, then the discount rate people are using to value Stock A must be higher. Put a different way, investors are demanding a higher expected return for holding Stock A.

This relationship is exactly what the value premium is getting at. Value stocks are stocks that have a low price relative to some proxy for their future cash flows (that fundamental metric that we mentioned earlier). So long as we accept the idea that different companies have different expected returns, then there has to be a value premium – the only question is how big that premium is, and how volatile it will be.

I want to dig into this question of how volatile the value premium is in practice, and specifically how often the value premium hasn’t come through. While we can talk about an expectation of a positive value premium, it is important to keep in mind that this premium only exists because value stocks are riskier than growth stocks. The value premium is the market’s inducement for people to hold these riskier stocks.

And because this is all based on risk, it isn’t unusual for growth stocks to outperform value stocks, though we are in a particularly bad period for value stocks. To put this in perspective, let’s look at some numbers.

Form July 1926 through November 2020 the annual average return for the value premium[1], which measures the returns of value stocks minus the returns of growth stocks, was 3.96%, with a substantial standard deviation of 12.14%. But how likely was the value premium to be negative?

To answer that, we can look at rolling returns. This type of approach steps through the returns, month by month, and looks at each subsequent period in turn. You can see the results below.

| Period Length | Percent of observations that were negative |

|---|---|

| 1 Year | 39.4% |

| 3 Years | 29.0% |

| 5 Years | 20.5% |

| 10 Years | 8.8% |

| 15 Years | 3.7% |

As you can see, it’s pretty normal for growth stocks to beat value stocks, especially over shorter periods of time. If you to pick a random month, there’s been nearly a 40% chance that the value premium will be negative over the next year, and a little bit more than a 20% chance that it will be negative over the next 5 years.

That said, what we’re seeing now goes beyond what we have seen historically. Prior to the period ending in May 2017, we had never had a 15 year period where the value premium was negative.

What’s going on here? The question isn’t so much about whether the value premium existed in the past – the data is pretty conclusive on that count – but rather has something fundamentally changed to cause the value premium to fail going forward?

Let’s take apart some of the more prominent arguments that I’ve seen floating around about why value is “dead” and see if those reports have been exaggerated.

Too Many People Know About Value

One of the more common reasons people suggest for the poor performance of the value premium is simply that too many people know about it now. It’s too well known, and there is too much money chasing it, so the premium has been “arbitraged away[2].”

The idea here is that since people now know that there has been a historical value premium, they are more willing to hold value stocks. They don’t demand as high of an expected return as they used to demand to hold value stocks. This means that the forward looking expected returns for value stocks is lower (remember, as prices go up, expected returns go down). And because the expected returns are lower, negative returns will be more frequent.

There are two problems with this argument.

It’s actually perfectly reasonable to think that the expected return of the value premium – or any other premium – has changed over time. Investors are constantly changing their preferences, so it may very well be true that the premium has dropped (more on this later). The problem is that this might get at the relative attractiveness of the value premium (how’s that for a catch-22?), but it doesn’t explain why value has had such a bad decade and a half.

Prices, including the relative prices of value and growth stocks, move based on how new information squares with what the markets expected to happen next. The value premium would still have roughly a 50/50 chance of outperforming (or underperforming) it’s “true” value.

We get to the second problem if we push a little further and argue that the expected return of the value premium is actually negative now. This would certainly explain why value stocks have done so badly for so long, but the problem with this argument is that markets just don’t work this way. Basically, why would anyone be willing to hold a security they expect to lose money relative to a less risky security? Presumably, the prices would drop to the point that someone thought there was a reasonable positive expected return to holding value stocks. At which point we would be back to “normal,” just at a lower price level.

Markets are constantly repricing risk, but that doesn’t explain what we’re seeing with value.

Intangible Assets Did It

Another common suspect is the changing nature of business, and specifically the rise of intangible assets. Intangible assets are, the argument goes, inherently difficult to value, and therefore we can’t measure value as effectively.

Before we dig in, let’s pause for a minute and talk a little bit about intangible assets. Intangible assets are assets that are, well, intangible. They aren’t a physical thing, like a piece of land or a machine. Intangible assets are things like brand recognition or intellectual property.

For our purposes, there are two types of intangible assets: internally created assets, and externally acquired assets. This is important because, while it is difficult (though not impossible) to put a value to internally created assets, we do have a pretty good value for externally acquired assets. That value is the price the company paid to acquire the asset – just like any other type of asset – and that fits nicely on a balance sheet.

So let’s focus in on the internally created assets. Is there a story there? Not really.

To give you a sense of why that is, here’s a chart of the weight of internally created intangible assets on company balance sheets, scaled by assets, from July 1962 through December 2018[3].

There is certainly a slight upward trend, but there’s not much there. In fact, as of 2018, internally created intangible assets had roughly the same weight on company balance sheets as they did back in the 80’s. You might be able to make a case that intangible assets changed how things worked moving from the 60’s to the 80’s, but that effect has already happened. There’s nothing that would seem to indicate we should be feeling an effect now.

FAANGS Will Eat Us All

Another avenue of attack against value is that the issue isn’t actually so much value versus growth stocks, but rather that a small group of very large companies are driving the returns of the market. Especially because of everything moving online because of the pandemic, it certainly feels like the FAANGs (Facebook, Apple, Amazon, Netflix, and Google/Alphabet), and big tech companies generally, are taking over[4].

But this argument has been floating around pretty much forever, and is actually more of a consequence of algebra than anything else. Just like with intangibles, not much has actually changed through time. There have always been a small group of huge companies that drive the returns of the market (which are almost by definition going to be growth companies). When those companies move, they’re going to drag the rest of the market along, simply because they are so big and represent a (relatively) huge proportion of the market’s total value.

All the way back in 2016 – when there was only one A in FAANG – Cliff Asness at AQR put together some data showing just how big of an impact the largest names have had on the S&P 500 Index going all the way back to 1994[https://www.aqr.com/Insights/Perspectives/SNAFU-Situation-Normal-All-FANGed-Up]. This isn’t driving the recent underperformance of value relative to growth, or at least no more than it always has been a drag on value stocks.

So what is going on?

Risk is Risky

People like comprehensible stories. We want to feel like the world is understandable, and that there are specific, tangible, reasons that we can point at to explain why things happen the way that they do. But that’s not always how the world works. Sometimes bad things happen, and then keep happening, simply by chance. That’s what’s been happening with the value premium now.

The value premium is having a historically bad run, but that’s what risk means. If we didn’t have periods like this one, it wouldn’t be risk. The market wouldn’t need to compensate us for holding the riskier value stocks. Right now, we are earning that value premium.

One of the important things to consider is how the value premium is inherent in our understanding of how not just the financial markets, but finance as a whole, works. There are premiums, such as the size premium, that you can think of as more empirical – we look to the size premium because of the data, not because of some theoretical argument that it needs to be there. I can easily imagine a world where small stocks weren’t necessarily more or less risky than large stocks, simply because those companies were smaller. And in fact, there is a growing body of research suggesting that the size premium isn’t truly a premium in and of itself. According to this research, size is more of an amplifier for other premiums[5].

But I have a lot more trouble imagining a world where low relative price stocks (value stocks) aren’t riskier than high relative price stocks (growth stocks). For this to be the case, our understanding of how to value securities needs to be seriously flawed. And this fundamental difference in risk between growth and value stocks is exactly what leads to the value premium.

While we may not know when Fortuna will decide that we’ve finally had enough, there are some promising rays of sunlight breaking through the clouds with regard to what we might be able to expect from the value premium in the future.

What’s the Spread?

Before we get into these glimmers of sunlight, it’s important to stress that we really can’t predict what the markets will do with any specificity. In any given year I expect value stocks to beat growth stocks. That’s true this year, it was true last year (that prediction didn’t work out so well), and it will be true fifty years from now. But we obviously know that all of these predictions can’t be correct, and we have no way of knowing when value stocks will lose, or when they will stop losing.

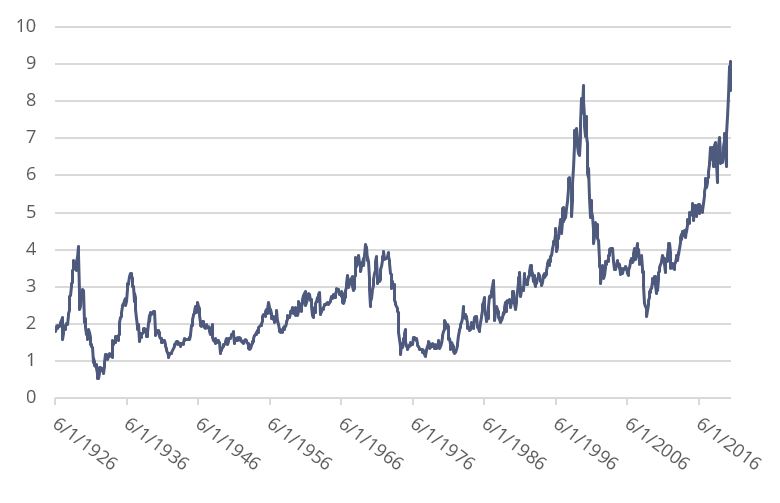

But there are some reasons for optimism about the value premium. A big reason to be optimistic is the spread between the Price to Book ratios of value and growth stocks. This spread is one of the ways that we can get some sense of what the current expected return of the value premium is. The bigger the spread, the higher the expected return of the value premium. And right now, the spread is as big as it’s ever been since 1926.

Spread Between the P/B of US Growth and Value Stocks

We haven’t seen spreads even close to this since the last days of the tech book. Now, I want to be careful here – this does not mean that we are guaranteed some massive value premium to “make up” for all of the bad returns we’ve gotten. It doesn’t even mean that we will necessarily have a positive value premium in the next couple years. This is all based on risk, and we’ve had a pretty sizable spread for a while now.

But it does mean that the expected return of the value premium is likely higher than it’s ever been. If you were comfortable with the value premium in the past, the arguments in favor of the value premium would seem to be even more convincing. Essentially, we’ve taken all of the pain, so we want to make sure that we stay positioned to capture the gain from the value premium.

The market is always looking forward. The past doesn’t matter, except in so far as it informs what the future could look like. We need to take the same approach with our portfolios. Just because value has seriously underperformed doesn’t mean that the market “owes us” anything. But it also doesn’t mean that value is dead either. We need to be continually reevaluating our portfolios and working to make sure that they are positioned to give ourselves the best chance to capture the returns the market is putting on offer so that we can reach our retirement goals.

And there is every reason to believe that the value premium will be a big part of that going forward.

[1] As measured by the Fama/French US Value Factor

[2] Yes, this isn’t actually arbitrage, but that’s what a lot of people call it.

[3] Data from Dimensional Fund Advisors. Following Peters and Taylor (2017), internally developed intangible capital for each firm at a point in time is estimated by accumulation the historical spending on research and development (R&D) and a fraction of selling, general, and administrative (SG&A) expenses while amortizing it at constant rates.

[4] A la Judge Dredd

[5] These arguments are very interesting, and I think there might be something to them, but they largely get us to the same place as if we consider size a true premium – all else equal, small stocks are riskier than big stocks and they have higher expected returns. The question is just how that risk and return is created.

McLean Asset Management Corporation (MAMC) is a SEC registered investment adviser. The content of this publication reflects the views of McLean Asset Management Corporation (MAMC) and sources deemed by MAMC to be reliable. There are many different interpretations of investment statistics and many different ideas about how to best use them. Past performance is not indicative of future performance. The information provided is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy or sell securities. There are no warranties, expressed or implied, as to accuracy, completeness, or results obtained from any information on this presentation. Indexes are not available for direct investment. All investments involve risk.

The information throughout this presentation, whether stock quotes, charts, articles, or any other statements regarding market or other financial information, is obtained from sources which we, and our suppliers believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in the transmission there of to the user. MAMC only transacts business in states where it is properly registered, or excluded or exempted from registration requirements. It does not provide tax, legal, or accounting advice. The information contained in this presentation does not take into account your particular investment objectives, financial situation, or needs, and you should, in considering this material, discuss your individual circumstances with professionals in those areas before making any decisions.