Ignore the Financial Media

WHAT IS OCCAM’S RAZOR? Occam’s Razor is a principle attributed to William Occam, a 14th century philosopher. He stressed that explanations must not be multiplied beyond what is necessary. Thus, Occam’s Razor is a term used to “shave off” or dismiss superfluous explanations for a given event. This concept is largely ignored within the investment management landscape. This newsletter will “shave off” popular investment misinformation and present what is important for achieving long-term investment success.

The financial media is omnipresent. Whether it’s hearing about what the Dow did today on your drive home, or a talking head pontificating about how the market’s are obviously about to tank, we are constantly immersed in a miasma of prognostication. Everyone has a take on what the markets will do next, and what you should do about it now. Whether that take has any relation to reality or not doesn’t seem to have much relevance. And unlike pre-game shows, no one is keeping track of how their analysts picks have done throughout the season.

But here’s the thing – people are obviously paying attention to all of the noise coming from the financial media. If there wasn’t an audience for this type of stuff, the financial media would go about things differently. They are, after all, businesses, so it’s worth thinking about their incentives, and how they drive what the financial media produces.

Incentives Matter

What are the financial media’s incentives? Not to put too fine a point on it, but they are there to make money. They do this by monetizing your attention. The vast majority do this by selling ads (of one form or another), though some still use a traditional subscription model on top of (or sometimes in place of) the ads. Essentially, if you aren’t paying attention, they aren’t making money. To a very large degree, you are the product.

And the easiest way to get attention is sensationalism. They need to be constantly heightening the tension. Whether they are telling us that the market is about to take off, and here’s what to do to capitalize on it, or that the market is about to take a disastrous turn and here’s how you must protect yourself, they want you to be nervous. They want you to feel like you need to know what will happen next – and they just so happen to be here to tell you what that is going to be.

The goal here is not to give you bad information. The goal is to keep you around for the ads. The vast majority of reporters want to try and help their readers and viewers, but their incentives make it hard to do that.

Shocking, sober, rational, and measured analysis does not sell.

Imagine how poorly a financial magazine would do if it’s cover had headlines like:

- Buy and Hold Now!

- 4 Tricks to Diversify Your Portfolio Today!

- We Don’t know Which Way the Market Will Go – And Here’s What You Should Do About It

While these would be practical articles for most people, no one would buy it. Even worse, they would only need to print one issue; there’s only so many ways to say that diversification is a good thing and that you need to focus on the long-term.

Instead, we get pundits making wild, short-term, calls. After all, even at the level of the individual pundit, there’s a lot of money in being the one who called the next 2008, and no one really cares how many times you get it wrong prior to that. To get a taste of this I pulled a couple of representative examples – so let’s take a look at how they did.

Back in 2016 Fortune ran an article entitled “6 Reasons You Should Be Extra Worried About the Market Right Now.” It’s even complete with a moody shot of the New York Stock Exchange building.

This is an article that could be written that comes out pretty constantly – they just swap out the reasons to match up with whatever everyone is currently worrying about (and we’re always worried about something). But let’s check how accurate this version happened to be.

The article was published on August 30th, 2016. In the year following it’s publication the S&P 500 Index was up 12%. If we were to expand the time period to the end of June 2019, the S&P 500 is up a little more than 35%. I’ll go out on a limb and say that this did not turn out quite like the author expected.

The media also loves to report on other people making bold predictions. Here we have an example, also from 2016, of “legendary billionaire investor Stanley Drunkenmiller” (I’m quoting from the article here) saying that you should sell stocks and buy gold.

So how good was this prediction? Not so great. In the year after the article was published (May 4th 2016 to May 3rd 2017) the S&P 500 Index was up about 16%, and gold was down about 3%. If we call it a longer term call (which is a pretty charitable reading) gold actually has gone up as of the end of June 2019. Since the article was published, gold is up nearly 10%. Problem is, the S&P is up more than four times more. The S&P 500 Index is up over 43%. I think I’ll stick with the market, rather than gold.

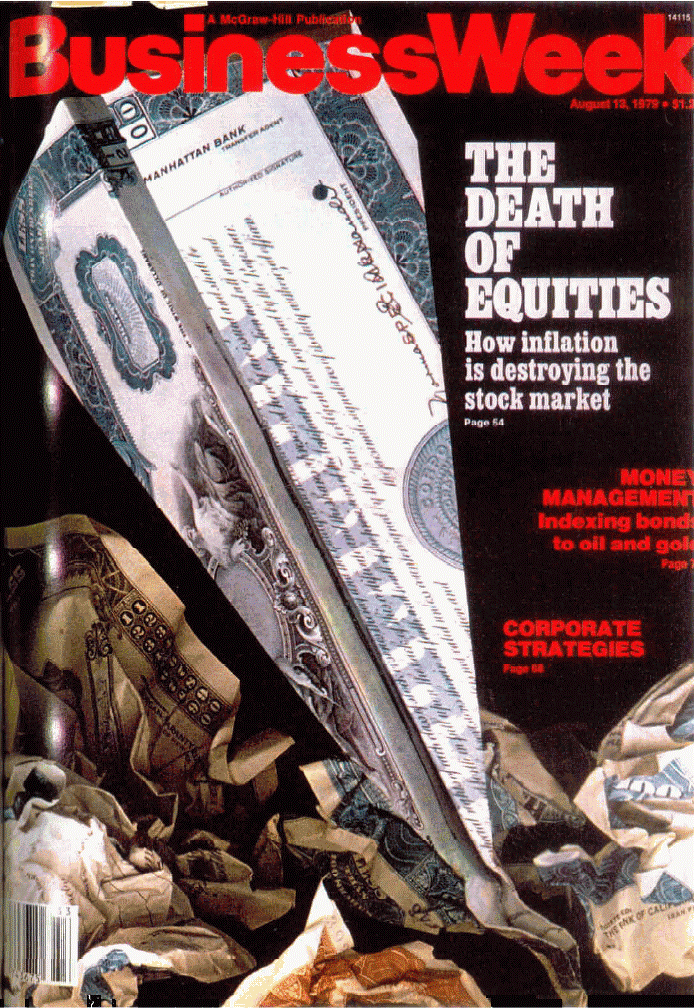

The classic of the genre though is a Business Week cover from August 1979. I’m pretty sure I’m not allowed to write this article without mentioning it. This is the famous “Death of Equities” article.

The article argued that because of high inflation stocks didn’t stand a chance. To put it mildly, this didn’t quite stand up over time. From August 13, 1979 (the day after the article was published) to the end of June 2019, the S&P 500 Index was up 2,639%. To put that in perspective, this equates to an annualized return of 8.3% over that time period. I wouldn’t mind my portfolio dying like that over the next 40 years.

One thing that I want to make sure that you notice is that all of these articles made perfectly reasonable cases. If you read through these articles you’d probably agree with most of their underlying arguments. But they consistently fall down in the same way – they all assume that the market hasn’t really absorbed the arguments that they’re making.

Take the Business Week article. It’s easy why, in the era of stagflation, people would assume that the stock market would be taking a hit. But we have to remember that the market moves based on new information, and specifically how that new information squares with what the market expected. And the market already knew about stagflation. That was already in the prices.

You Can’t Beat The Market

As we all know, making predictions is hard– especially about the future. The examples I pulled here were all flops (to put it mildly), but just as easily I could have pulled predictions that did end up working out. In fact, these predictions are roughly as accurate as a coin flip. The market is basically as likely to go up as it is to go down in the short-term, and this is exactly the point.

All of this is just noise. The information that the financial media is using to make their predictions has already been absorbed by the markets. Just like always, what happens next – and how that squares with what the market expected – will drive markets.

We see this very clearly when we look at actively managed funds (where they do track how people have done with their predictions). If we look at what are called persistence studies, it becomes very clear that active managers aren’t adding any value for their investors.

The idea here is that if a manager can beat the market through skill, rather than luck, then the managers that beat the market in one period should be able to beat the market in the next period, at least on average. Or at the very least, they should do better than the average manager, but this isn’t how the data shakes out. The data shows that active managers who beat the market in one period are not much more likely to beat the market in the subsequent period. It’s largely just pure, dumb luck (and even when it’s not – like with Peter Lynch – it’s not really transferrable.)

There have been some big name reporters who have made the jump from pundit to fund manager. The biggest to do so is probably Ron Insana. In the early 2000’s, Insana was one of the biggest stars in the financial media, and he decided that rather than just report on what the market would do next, he was actually going to make some money on that information. In March 2006, he founded Insana Capital Partners, and opened a hedge fund called the Legends Fund.

The Legends Fund was a fund of funds, which means that he was picking other managers that he thought would beat the market to put his investor’s money into. Now, he obviously didn’t do this for free. He charged his investors 1.5% of their assets with him every year, as well as 20% of the profits that the fund made. And remember, this is on top of the fees that the underlying funds that the Legend Fund invested in charged.

The fund only lasted about two years. It shut down in August of 2008. Insana is currently a contributor at CNBC.

This is Dangerous For Retirement Income Investors

It’s easy to point and laugh at what the financial media is doing, but it’s really not funny. It’s dangerous. People believe what they hear, especially since nearly everyone in the media is saying some version of the same thing, and this is putting a lot of people’s retirements in jeopardy.

It would be one thing if all of this noise simply went in one ear and out the other, if it were simply less interesting celebrity gossip. Unfortunately, that’s not the case. People trade on this stuff, and it’s hard to blame them. Most people simply don’t know better.

People take the “best” advice that they can find and smash it all together. Since most of the media roughly agrees that it’s possible to beat the market (so long as you listen to their channel), most people think that it’s a matter of picking the best “expert” to follow. Then, most people end up cycling through a number of these “experts.” The first one they picked worked for a while, and then she started to taper off, so you start listening to someone else. This next one had a rough quarter, so obviously they didn’t know what they were talking about…And the cycle continues. What this means is that most people end up owning a lot of “stuff.” In a lot of cases it’s a stretch to even call it a portfolio. It’s like the finance industry’s junk drawer exploded.

As you might imagine, this doesn’t work very well.

But again, this isn’t completely the fault of the investor. While the information on how to invest effectively is out there (here, for instance), most people just don’t know where to look. The financial media is ubiquitous, and everyone is singing from the same songbook. Why would they look elsewhere?

Investors are in a bad situation, and the financial media is actively reinforcing the things that don’t work.

So, what should you do?

Now that I’ve painted such a bleak picture, what should we do about it? Well, the first thing to do is to stop paying attention to the financial media. This is easier said than done, but it’s important. Even when you understand what they’re doing, the financial media is really good at getting you firmly aboard the fear vs greed roller coaster (it is their job after all.)

Your goal should be to get off and stay off this rollercoaster. You want to be on the line in the middle. There aren’t the ecstatic highs, but there are aren’t the crushing lows either. The middle line may be boring, but it’s a lot more likely to get you where you want to go.

What does it take to get off of the rollercoaster?

It takes a solid understanding of three things:

- How the markets work

- How much risk you can tolerate

- What you are trying to accomplish with your portfolio

This first point is a little bit like the table stakes. More than knowing the mechanics of how the markets operate (though that is helpful), what you really need to understand is that the market is smarter than any one person. We should be focused on harvesting the long-term returns that the market offers us – if we stay disciplined.

The second thing you need to understand is how much risk you can tolerate in your portfolio before you wake up in a cold sweat worried about your retirement. It’s easy enough to say that to get the best returns you need to take a huge amount of risk, and that the markets tend to reward investors who stick it out. But that last part about sticking it out is the rub here. Would you be able to “stick out” another 2008? How about something worse? Most people wouldn’t be able to. So you need to think about what portfolio will work for you. What is your appropriate amount of risk? A good way to think about this is to ask yourself “How am I different from the average investor?”

And last, but certainly not least, you need to understand what you want out of your portfolio. If you’ve already got all the money you need to have a great retirement, well, you don’t really need that much from your portfolio. You don’t have to take much risk. On the other hand, if you have a big gap to cross to get to the retirement that you want, you may need a more aggressive portfolio (or you could rethink what you want out of retirement).

The financial media desperately wants you to think that investing is rocket surgery. But it’s really not. Investing for retirement is straightforward. Mind the things that you can control, stay off the fear vs greed roller coaster, focus on the long-term, and you’ll position yourself to have a great investment experience.

McLean Asset Management Corporation (MAMC) is a SEC registered investment adviser. The content of this publication reflects the views of McLean Asset Management Corporation (MAMC) and sources deemed by MAMC to be reliable. There are many different interpretations of investment statistics and many different ideas about how to best use them. Past performance is not indicative of future performance. The information provided is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy or sell securities. There are no warranties, expressed or implied, as to accuracy, completeness, or results obtained from any information on this presentation. Indexes are not available for direct investment. All investments involve risk.

The information throughout this presentation, whether stock quotes, charts, articles, or any other statements regarding market or other financial information, is obtained from sources which we, and our suppliers believe to be reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in the transmission there of to the user. MAMC only transacts business in states where it is properly registered, or excluded or exempted from registration requirements. It does not provide tax, legal, or accounting advice. The information contained in this presentation does not take into account your particular investment objectives, financial situation, or needs, and you should, in considering this material, discuss your individual circumstances with professionals in those areas before making any decisions.